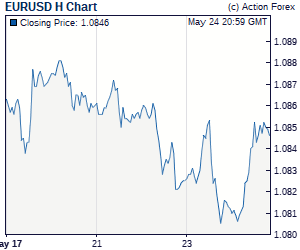

European majors are trading generally higher today as Eurozone will take the center of stage. There are worries of deeper and longer than expected slowdown in the Eurozone economy. PMIs from Germany, France and Eurozone will provide some hints on economic performance at the start of the year. ECB rate decision will for sure be the focus too. In particular, the tone of the post-meeting press conference will likely turn more cautious, if not dovish. Hence, while Euro is recovering, there is risk of renewed selling ahead, which might also drag down the Swiss Franc and, to a lesser extent, Sterling. European majors are trading generally higher today as Eurozone will take the center of stage. There are worries of deeper and longer than expected slowdown in the Eurozone economy. PMIs from Germany, France and Eurozone will provide some hints on economic performance at the start of the year. ECB rate decision will for sure be the focus too. In particular, the tone of the post-meeting press conference will likely turn more cautious, if not dovish. Hence, while Euro is recovering, there is risk of renewed selling ahead, which might also drag down the Swiss Franc and, to a lesser extent, Sterling. On the other hand, commodity currencies are generally lower despite lack of risk aversion in the markets. Australian Dollar turns south after mixed job data, strong in the headline by questionable in the details. New Zealand Dollar is paring some CPI prompted gains. Meanwhile, Canadian Dollar weakens as oil recovery lost momentum. Technically, AUD/USD's break of 0.7116 minor support today suggests that the rebound from flash crash low at 0.6722 has completed at 0.7235 already. More downside is now in favor in AUD/USD to retest 0.6722 low. Sterling's rallies against Dollar, Euro and Yen are in progress, still with firm intraday momentum. EUR/USD is in recovery while USD/CHF is in retreat. But there is no change in near term outlook. That is, more upside is in favor in Dollar against Euro and Franc. In other markets, Nikkei closed down -0.11% today. At the time of writing, Hong Kong HSI is up 0.28%, China Shanghai SSE is up 0.47%. Singapore Strait Times is up 0.37%. Japan 10 year JGB yield is up 0.0031 at 0.0009, staying positive. Overnight, DOW rose 0.70%. S&P 500 rose 0.22%. NASDQ rose 0.08%. 10-year yield rose 0.025 to 2.744. |

No comments:

Post a Comment