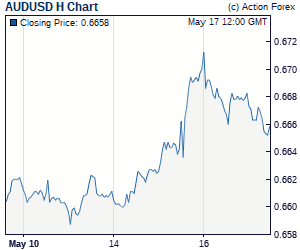

Selloff in New Zealand and Australian Dollar is the main theme in Asian session today. Kiwi plummets after RBNZ stands pat and indicates that the next move is a cut. After that, a full RBZN cut in priced in November but there are speculations on as early as a May cut. At the same time, RBNZ's dovish seems to be adding to the case for RBA to cut twice this year too. For now, more downside are expected in both currencies for the near term. Selloff in New Zealand and Australian Dollar is the main theme in Asian session today. Kiwi plummets after RBNZ stands pat and indicates that the next move is a cut. After that, a full RBZN cut in priced in November but there are speculations on as early as a May cut. At the same time, RBNZ's dovish seems to be adding to the case for RBA to cut twice this year too. For now, more downside are expected in both currencies for the near term. Meanwhile, Yen and Dollar are the strongest ones, followed by Euro. The greenback is partly helped by weakness in other major currencies, and rebound in stocks overnight. But upside of Dollar is capped by yield curve inversion so far. 10-year yield dropped for another day to 2.414 overnight and 2.4 handle now looks vulnerable. Inversion with 3-month yield (now at 2.464) will only get worse before getting better. Technically, EUR/USD's fall from 1.1448 resumed by breaking 1.1273 temporary low and it should be heading to 1.1176 key support level. EUR/CHF also resumed fall from 1.1444 but it's trying to draw support from key support zone at 1.1154/98. Sterling will be a key so focus today and Brexit alternative votes loom in Commons. It's so far stuck in range against Dollar, Euro and Yen. 0.8474 support in EUR/GBP is the level to watch for Sterling strength. 1.2960 in GBP/USD and 143.72 in GBP/JPY are the levels to watch for Sterling weakness. In Asia, Nikkei closed down -0.23%. Hong Kong HSI is up 0.62%. China Shanghai SSE is up 0.59%, back above 3000 handle. Singapore Strait Times is up 0.34%. Japan 10-year JGB yield is down -0.027 at -0.068. Overnight in US, DOW rose 0.55%. S&P 500 rose 0.72%. NASDAQ rose 0.71%. 10-year yield dropped -0.006 to 2.414. |

No comments:

Post a Comment